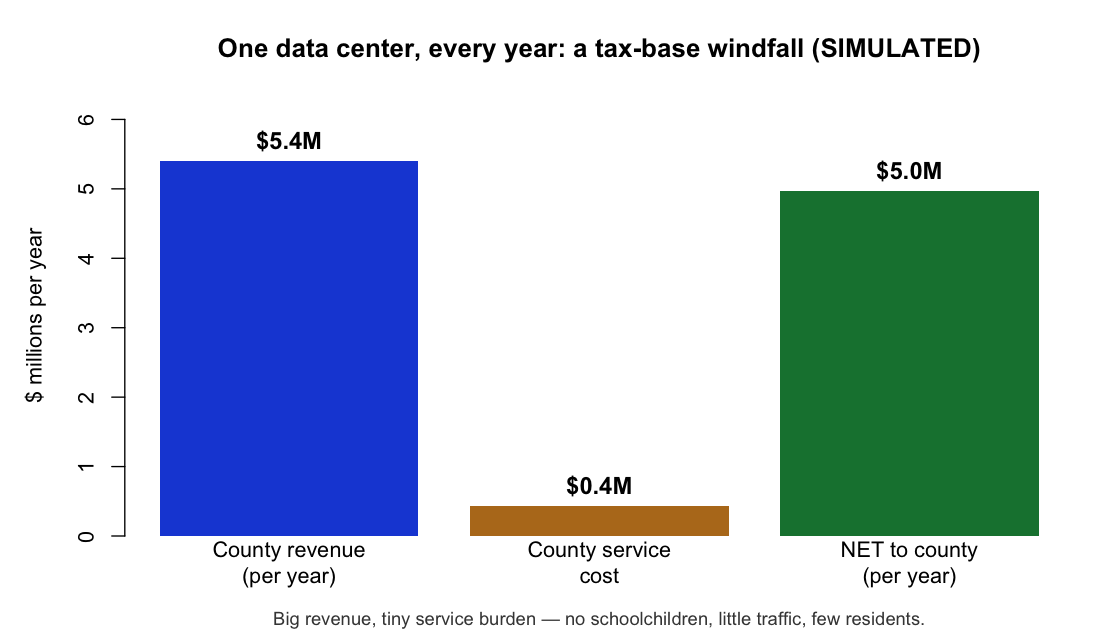

A data center pays in — and barely draws down

Unlike housing, a data center adds a large taxable asset with almost no demand for county services. In our illustrative campus that's ~$5.4M/yr in property tax against ~$0.4M of services — a net ~$5.0M/yr. (Loudoun County, VA: ~38% of general-fund revenue from ~4% of land, a decade of residential tax cuts.) The R that sets it up:

# SOURCE: county assessor + budget records (illustrative campus parameters) assessed_val <- 0.60e9; tax_rate <- 0.009 # one hyperscale campus gross_rev <- assessed_val * tax_rate # ~$5.4M/yr to the county net_rev <- gross_rev - 0.08 * gross_rev # ~$5.0M/yr after services

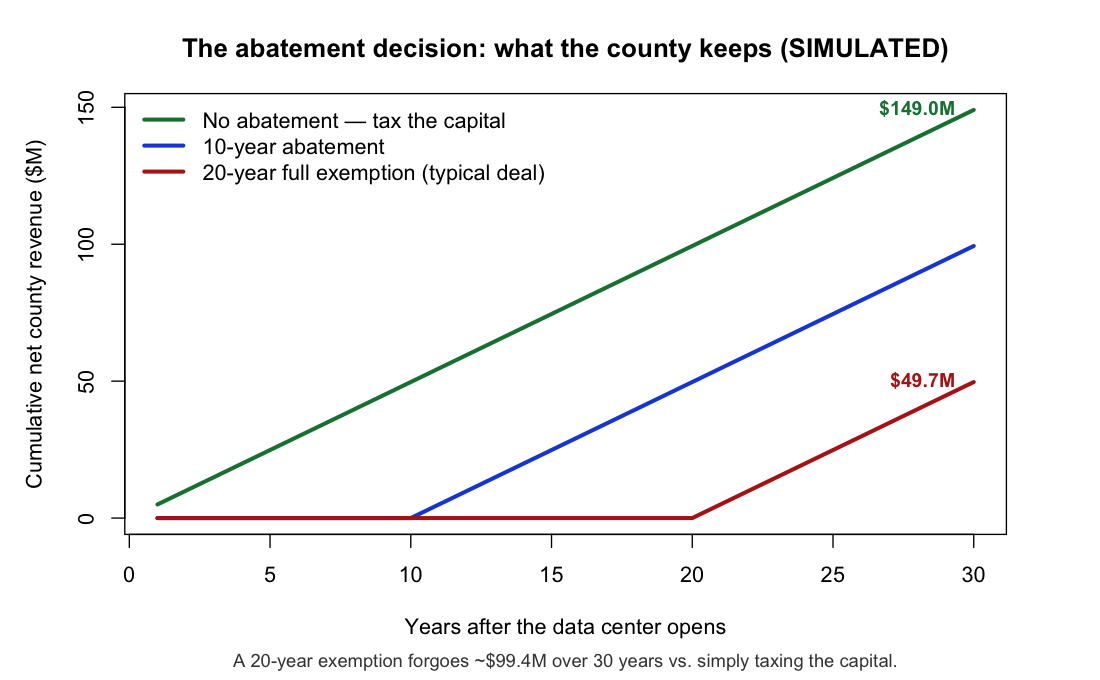

data/raw/SOURCES.mdThe abatement is what you actually vote on

The plant is good for the county whether or not you abate its taxes — so the vote is really about the abatement. This is what the county keeps under each choice; the gap between the lines is money handed back. A six-line function generates all three scenarios:

# Cumulative net county revenue under an A-year property-tax abatement cum_rev <- function(A) cumsum(ifelse(seq_len(30) <= A, 0, net_rev)) keep_taxed <- cum_rev(0) # tax the capital from day one -> ~$149M keep_20yr <- cum_rev(20) # 20-year full exemption -> ~$50M

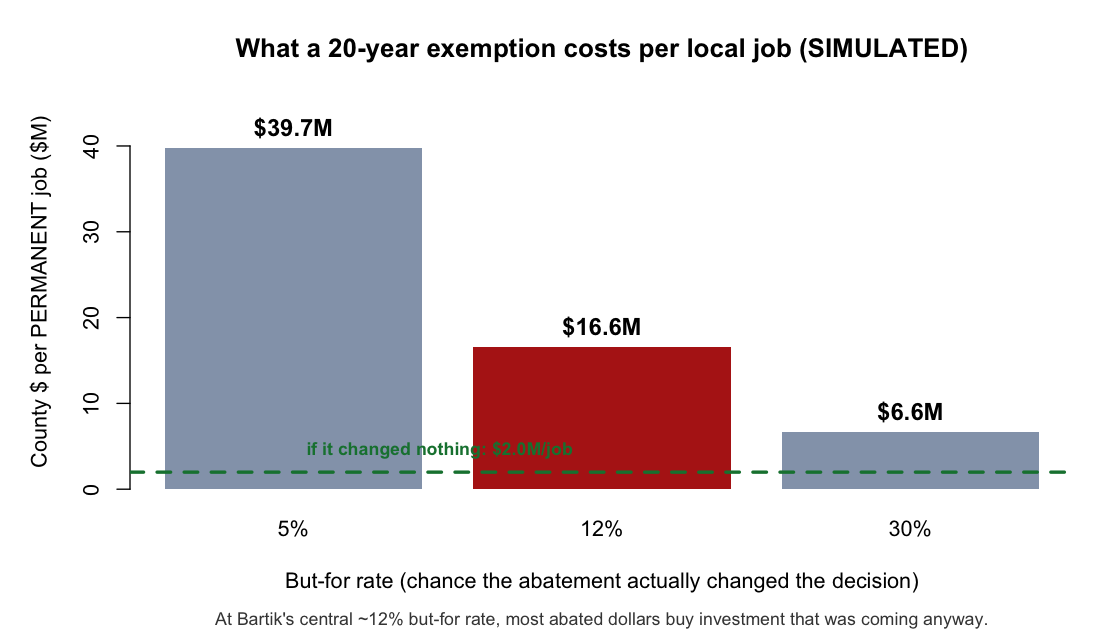

data/raw/SOURCES.mdPer local job, an open-ended exemption is hard to justify

This isn't a knock on the data center — it's about the terms. Spread the abated revenue over the handful of permanent jobs and the price per job is steep, and steeper once you weight by the but-for rate. At Bartik's central ~12%, most abated dollars buy investment that was coming anyway:

# SOURCE: Bartik (2018) but-for rate ~12% — the share of decisions an incentive tips forgone_20 <- net_rev * 20 # county $ given up over a 20-yr exemption per_job <- forgone_20 / 50 # only ~50 permanent on-site jobs -> ~$2.0M per_induced <- per_job / 0.12 # per job the abatement actually caused -> ~$16.6M

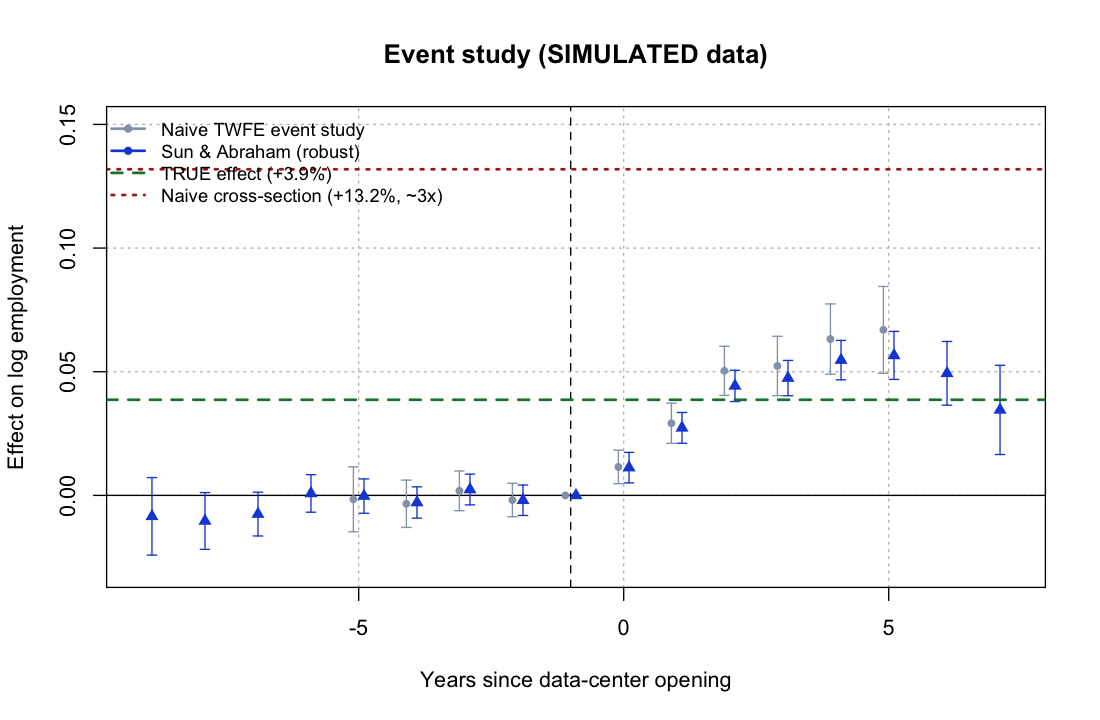

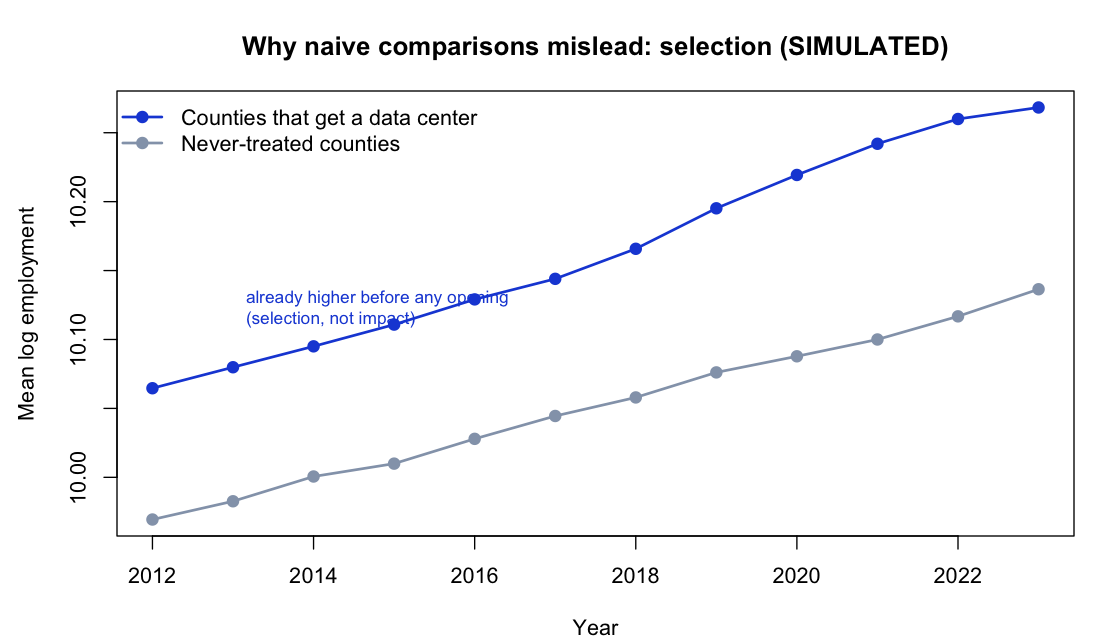

\citep{bartik2018butfor}Don't bank on a “jobs boom” — bank on the tax base

Boosters promise a wave of indirect jobs. Be careful: because data centers are sited in counties already growing, a naive before/after comparison overstates the employment effect ~3×. A proper event-study estimator in R strips that selection out and finds a real but modest effect. The bankable prize is the tax base.

# Don't bank on a "local boom": does it survive a real estimator? library(fixest) naive <- feols(log_emp ~ i(treated_ever), subset = year == 2023) # +13.2% robust <- feols(log_emp ~ sunab(cohort, year) | fips + year) # +3.8% (true +3.9%)

\citep{baharwright2026}

This is the paper's cost-benefit core in miniature: the investment (Ledger A — a low-service-burden tax base, vivid in the Loudoun case) vs. the firm-specific subsidy (Ledger B — mostly inframarginal at a ~12% but-for rate). The verdict — welcome the plants, question the abatements — and the cost-per-induced-job math come from §8–§9. The economic case → · Read the paper →

Rscript code/R/demos/demo_county_fiscal.R and demo_event_study.R (base R; fixest for the event study). All numbers simulated from labeled assumptions for illustration only. · Project hub · The paper